TL;DR:

- Yes, you can sell a car before finishing its payments — but the loan has to be settled first. A buyer's deposit isn't a settlement, and a verbal promise from the seller isn't a release.

- The process has a fixed order: request a settlement figure from your bank, pay off the balance, receive a release letter (NOC), then transfer ownership through the usual channels.

- Paying off early is usually allowed and, under murabaha-style financing, can reduce the total profit charged — ask your bank for the exact early-settlement terms on your contract.

- Buyers should never hand settlement money to the seller. The payoff goes to the bank directly; only the leftover (if any) goes to the seller.

- Stop paying, and the car can be repossessed — the bank's interest in the vehicle doesn't disappear just because you've stopped making payments or gone quiet.

Quick answer: A car with outstanding bank financing can be sold, but the loan must be settled before ownership transfers. Request a settlement (payoff) figure from your bank, pay the remaining balance, and receive a release letter or no-objection certificate (NOC) confirming the bank's interest is cleared. Only then can the Istimara be transferred to a buyer through the normal ownership-transfer process. Buyers should always verify a car's finance status and insist on seeing the release paperwork before paying anything toward the purchase.

How car financing actually works here

Most car finance in Saudi Arabia runs on a murabaha structure: the bank or financing company buys the car (or pays the dealer) and sells it to you at a markup, which you repay in fixed installments over an agreed term. Until that agreement is fully settled, the financing company holds a real interest in the vehicle — practically, that means the car isn't fully "yours to sell" in the way a paid-off car is.

This matters because a lot of the confusion around selling a financed car comes from treating it like a normal private sale with an extra phone call to the bank. It isn't. The bank's interest has to be formally cleared — through a specific settlement process — before the ownership transfer that's covered in our car ownership transfer guide can go through cleanly. Think of this article as the step that happens before that one: get the finance cleared first, then the standard transfer mechanics apply.

Can you sell a financed car?

Yes — this is normal and financing companies handle it routinely. What you can't do is transfer ownership to a buyer while the bank's interest is still active, because the registration and the financing agreement are linked. The car can change hands in one of two ways: you settle the loan yourself (from savings, from the buyer's payment, or a mix of both) and then sell with a clean title, or — less commonly for private sales — the buyer's own bank pays off your existing loan directly as part of arranging their financing.

For most private sales, the simplest and safest path is: agree a price with your buyer, use part or all of that agreed amount to settle your loan with the bank, get your release letter, then complete the transfer and collect the rest of the payment. We'll walk through each piece below — and once your title is clean, the sale itself works exactly like any other listing on KSAplate.

Getting your settlement figure

The settlement (or payoff) figure is the exact amount needed to close out your financing agreement as of a specific date — it is not the same as simply adding up your remaining monthly installments, since the murabaha profit structure can front-load some of the profit and may be recalculated for early closure.

- Request it directly from your financing company — by phone, branch visit, or through their app/portal if they offer one. Give them the date you intend to settle, since the figure is time-specific and typically only valid for a short window.

- Get it in writing. A verbal number over the phone is useful for planning, but you'll want an official settlement letter or statement before you hand over any money, so there's no dispute about the agreed figure later.

- Ask about any early-settlement adjustment at the same time — some agreements reduce the profit portion for paying early, others don't; this varies by lender and by contract, so don't assume either way.

Build in a few days between requesting the figure and actually paying it — bank processing isn't instant, and if your settlement window expires you may need to request a fresh figure.

What's your car worth?

Get a free instant estimate based on real Saudi market data — then sell it on KSAplate with direct WhatsApp contact.

Value My Car — FreeEarly settlement: costs and savings

Because murabaha financing fixes the total profit at the start of the contract rather than charging interest that accrues daily, "paying it off early" doesn't always work the same way it would with a conventional interest-based loan. Some financing agreements rebate a portion of the unearned profit when you settle early; others charge the full agreed amount regardless of timing. Both structures are used in the market, and the difference is written into your specific contract — not into any general rule this article, or any other, can safely state for you.

The practical steps that protect you either way: read the early-settlement clause in your financing agreement before you commit to a sale price with a buyer, ask your bank to itemize the settlement figure so you can see whether a rebate has been applied, and factor the real payoff number — not an estimate — into what you actually need from the sale to come out even or ahead.

The release letter and ownership transfer

Once you've paid the settlement figure, the bank issues a release letter — sometimes called a no-objection certificate (NOC) or clearance letter — confirming the financing agreement is closed and the bank has no further claim on the vehicle. This document is what unlocks the rest of the process.

| Step | What happens | Who's involved |

|---|---|---|

| 1. Settlement figure | Bank confirms the exact payoff amount as of your chosen date | You + your bank |

| 2. Payment | You pay the settlement amount to the bank | You + your bank |

| 3. Release letter / NOC | Bank confirms in writing that its interest in the car is cleared | Your bank |

| 4. Ownership transfer | Standard transfer process — both parties present, Istimara updated | You, buyer, Absher/traffic authority |

| 5. Final payment & handover | Buyer pays the agreed price in full; keys and documents change hands | You + buyer |

Once you have the release letter, the transfer itself follows the same mechanics as any other sale — matching ID, both parties present or using an authorized power of attorney (wakala) if needed, and an updated Istimara in the buyer's name. Our ownership transfer guide covers that process step by step — this article's job is just to get you to a clean, unencumbered title before you start it.

Trade-in with outstanding finance

If you're trading the car in rather than selling it privately — for example, as part of buying your next car — dealers handle outstanding finance as a routine part of the transaction. Typically, the dealer's finance team contacts your bank directly, confirms the settlement figure, and deducts it from your trade-in value before calculating what you're credited toward the new purchase.

The habit worth keeping regardless: ask for the settlement figure yourself beforehand so you know what to expect, and get written confirmation once the dealer has actually paid it off — don't assume it's handled just because the dealer says so. Our trade-in vs private sale guide covers the broader trade-offs between these two paths in depth; the table below adds the outstanding-finance angle specifically.

| Private sale (finance settled by you) | Dealer trade-in | |

|---|---|---|

| Who contacts the bank | You | The dealer's finance team, usually |

| Typical net proceeds | Higher | Lower, but simpler |

| Time & effort | More — you manage settlement, buyer and transfer | Less — bundled into one transaction |

| Paperwork risk | On you — chase the release letter yourself | Lower — confirm in writing, but still verify |

| Best for | Sellers who want maximum value and can handle the steps | Sellers prioritizing convenience over price |

Once you've settled on a path, you can browse the marketplace for your next car while your current one is being sold or traded — comparing what a private sale nets you against a dealer's trade-in offer is easier once you know roughly what similar cars are listed for.

Buying a car: verifying there's no hidden finance

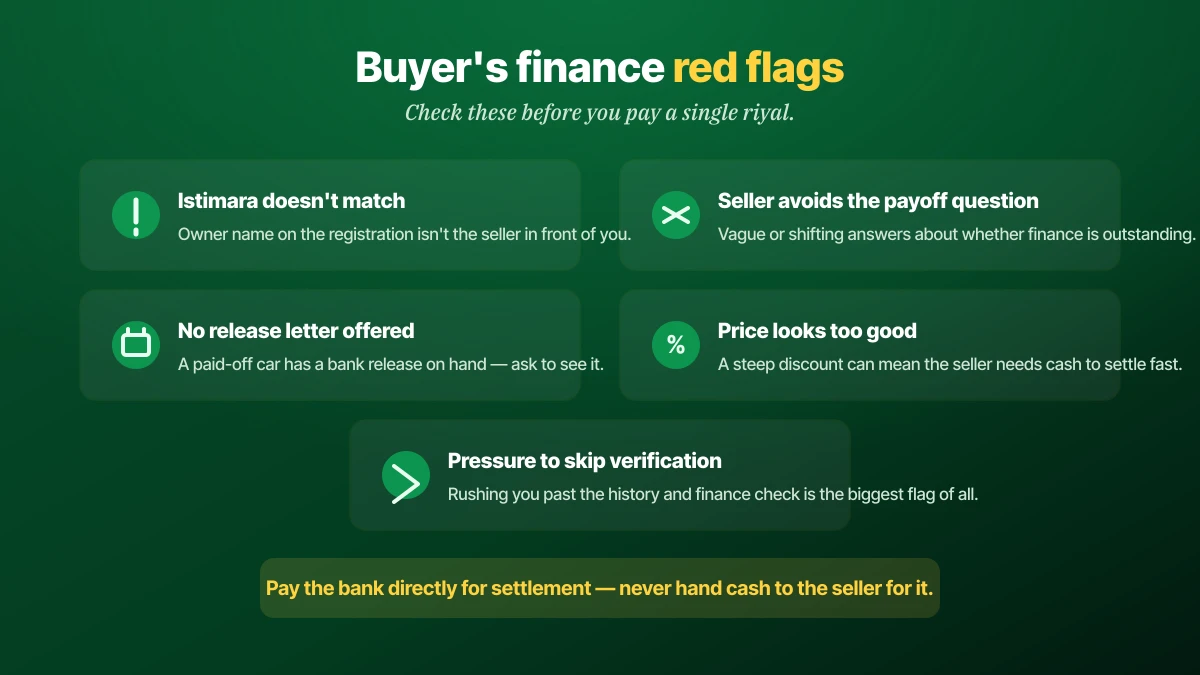

If you're on the buying side, the core risk is straightforward: paying a seller in full for a car that still has an active bank claim on it, then discovering the ownership transfer can't complete because the finance was never settled.

A few checks cover most of the risk. Confirm the name on the Istimara matches the person selling to you — a mismatch is the clearest sign something (a prior sale, a family transfer, or outstanding finance) hasn't been fully resolved. Ask directly whether there's outstanding finance on the car, and if there is, ask to see the settlement figure and insist the payoff happens before or simultaneously with your payment — never after. A vehicle history check is worth running alongside this, since finance status is exactly the kind of thing a rushed private sale can obscure, and the patterns overlap with what our used car scams guide flags more broadly. When in doubt, structure the payment so the settlement amount goes straight to the bank and only the remainder goes to the seller — this protects you from a seller who takes your money and never actually clears the loan.

What happens if you stop paying

The financing company's interest in the vehicle doesn't depend on you staying in touch — it depends on the contract. Missed payments typically move through reminder notices, then formal default procedures, and can ultimately lead to repossession of the vehicle, alongside the credit and financial consequences of defaulting on any loan in Saudi Arabia. None of this is a reason to avoid financing; it's a reason to talk to your bank the moment you know a payment will be late, rather than after you've already missed it — financing companies generally have more flexibility to work with a borrower who communicates early than one who goes silent.

If you're financially stretched and considering letting the car go rather than keep paying, selling it yourself — even at a modest loss after settlement — is almost always a better outcome than a missed-payment spiral ending in repossession, which tends to be more expensive and more damaging to your credit standing than a voluntary, orderly sale.

Financing, insurance and the registered owner

Financed cars still need standard car insurance in your name as the registered owner — financing doesn't change who's responsible for keeping the car insured, and a lapse in coverage is your problem to resolve, not the bank's. It's also worth keeping your own copy of the financing agreement, payment records, and eventually the release letter together with your other ownership documents; if a question ever comes up about the car's finance history — at resale, at a Fahes inspection, or during a dispute — having the paper trail on hand settles it faster than trying to request records from the bank after the fact.

Mistakes to avoid

The same handful of errors account for most of the friction and financial risk in this process.

- Agreeing a sale price before requesting a settlement figure. You need the real payoff number to know what you're actually netting from the sale.

- Treating a buyer's deposit as a settlement. The bank needs to be paid the full settlement amount before its interest clears — a partial deposit from a buyer doesn't do that.

- Selling on a verbal promise instead of a written release letter. Without the NOC in hand, there's no proof the bank's claim is cleared, and the transfer can stall.

- Buyers paying the seller in full before confirming the finance is settled. This is the single most common way buyers lose money in financed-car sales.

- Assuming a dealer trade-in automatically clears your finance. Get the settlement confirmed in writing rather than taking it on faith.

- Going quiet after a missed payment. Communicating early with your bank almost always produces a better outcome than avoidance.

- Letting insurance lapse mid-financing. You're the registered owner and responsible for coverage regardless of the loan status.

Frequently asked questions

Can I sell my car in Saudi Arabia if I still owe money on it?

What is a settlement figure and how do I get one?

Do I get money back for paying off my car loan early?

What is a release letter or NOC for a car loan?

Can I transfer car ownership before the loan is fully paid off?

How do I know if a used car I'm buying still has finance owed on it?

Should I pay the seller directly to settle their car loan?

What happens if I trade in a financed car at a dealership?

What happens if I stop paying my car loan in Saudi Arabia?

Do I still need car insurance while the car is financed?

Is it better to sell a financed car privately or trade it in?

Conclusion & next steps

Selling or buying a financed car in Saudi Arabia isn't complicated once you treat it as two separate steps done in order: clear the bank's interest first, then transfer ownership like any other sale. Request a real settlement figure, pay it, get the release letter in writing, and only then move to the standard transfer process. Buyers protect themselves the same way — verify the finance status, insist on seeing the release paperwork, and never pay a seller in full before the bank's claim is confirmed cleared.

If you're preparing to sell, start with an honest valuation so you know what the car is actually worth against your settlement figure, then follow our guide to selling a car for the rest of the process, and list it on KSAplate once your title is clean. Buying instead? Browse the marketplace with the questions from this guide in hand — Istimara match, finance status, release paperwork — and you'll avoid the one mistake that causes the most trouble in financed-car sales.