TL;DR:

- Car insurance is mandatory in Saudi Arabia — at minimum you need third-party liability (TPL) to drive legally and to renew your registration.

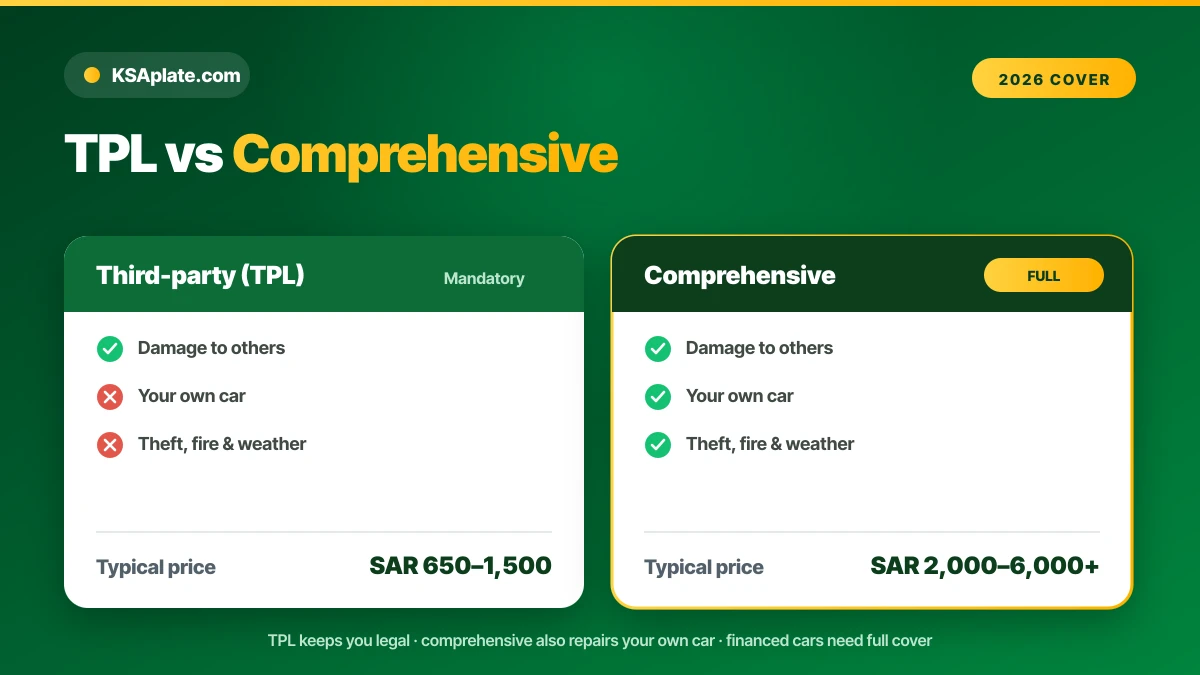

- TPL covers damage and injury you cause to others; it does not cover your own car. Comprehensive adds own-damage, theft, fire and weather.

- Prices in 2026: TPL from about SAR 650–1,500 a year; comprehensive roughly SAR 2,000–6,000+, depending on the car and your record.

- Buy online in minutes by comparing insurers on an aggregator like Tameeni; the policy issues instantly and is verified live in Absher and Tawakkalna.

- Accidents are reported and claimed through Najm. A financed car almost always requires comprehensive cover.

Quick answer: Car insurance in Saudi Arabia is legally required. The minimum is third-party liability (TPL), which covers harm you cause to others and starts around SAR 650 a year. Comprehensive insurance also covers your own car and costs more. You buy it online in minutes with your Iqama and istimara, and a valid policy is required to renew your vehicle registration.

What car insurance is in Saudi Arabia

Car insurance in Saudi Arabia is a legally required policy that protects against the financial cost of road accidents. Driving without valid cover is an offence, and a live policy is checked digitally through Absher and Tawakkalna. The market is regulated by the Insurance Authority, and every policy is recorded centrally, so the traffic system always knows whether your car is insured.

Insurance sits in the middle of the vehicle lifecycle. You need it to register a car, to renew that registration, and to transfer ownership. In practice, the question is not whether to insure but which level of cover to buy — the legal minimum, or full protection for your own vehicle.

Saudi Arabia runs one of the largest motor-insurance markets in the Gulf, with dozens of licensed insurers competing on price and service. That competition is good news for drivers: comparing quotes for the same car routinely reveals price gaps of hundreds of riyals, so a few minutes of comparison pays for itself every single year.

TPL vs comprehensive insurance

Saudi Arabia has two main types of motor cover. Third-party liability (TPL) is the mandatory minimum. Comprehensive is optional but far broader. The right choice depends on your car's value and how much risk you want to carry yourself.

| Feature | Third-party (TPL) | Comprehensive |

|---|---|---|

| Legally required | Yes — the minimum | Optional (often required if financed) |

| Damage to others | Covered | Covered |

| Your own car | Not covered | Covered |

| Theft & fire | No | Yes |

| Weather / floods | No | Usually yes |

| Typical 2026 price | SAR 650–1,500/yr | SAR 2,000–6,000+/yr |

TPL keeps you legal and protects other people. Comprehensive protects your car too — the difference is who pays when your own vehicle is damaged.

What TPL does not cover

Third-party liability is the most misunderstood product on the market. TPL pays for injury and damage you cause to other people, their vehicles, and their property — up to high statutory limits. It pays nothing toward repairing your own car. If you hit a wall, your engine catches fire, or the car is stolen, a TPL policy leaves you to cover the loss yourself.

That gap is the whole reason comprehensive exists. For an older, low-value car, many owners accept the risk and keep TPL. For a newer or expensive vehicle — or any car still being paid off — the maths usually points to comprehensive.

What's your car worth?

Get a free instant estimate based on real Saudi market data — then sell it on KSAplate with direct WhatsApp contact.

Value My Car — FreeHow much car insurance costs (2026)

The price of car insurance in Saudi Arabia depends mostly on the car and the driver, but the bands are predictable. TPL is cheap; comprehensive scales with the value of the vehicle it protects.

| Cover | Typical annual price (SAR) | Best for |

|---|---|---|

| TPL — economy car | ~650–900 | Older, low-value cars |

| TPL — larger car | ~900–1,500 | Legal minimum on any car |

| Comprehensive — mid-range | ~2,000–3,500 | Newer family cars |

| Comprehensive — premium / SUV | ~4,000–6,000+ | High-value & financed cars |

These are market ranges, not quotes. The only way to know your real price is to compare insurers for your exact car — which an aggregator does in a couple of minutes.

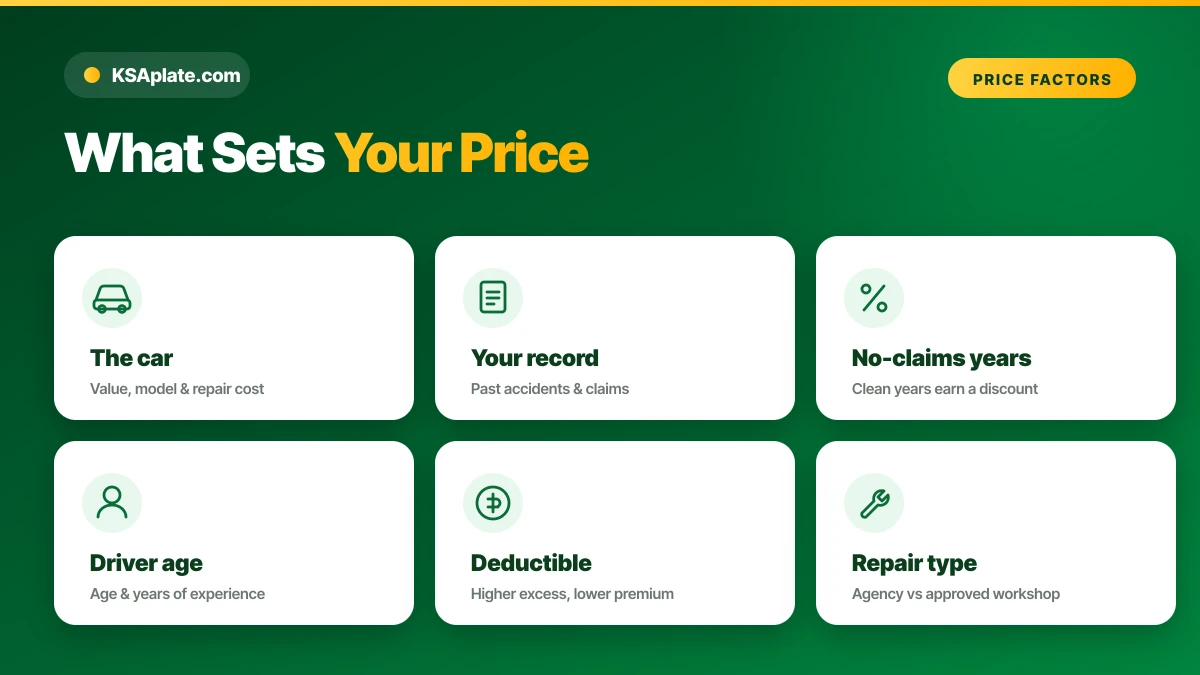

What affects your premium

Insurers price risk. A handful of factors move your premium up or down, and knowing them helps you lower the bill.

- The car — make, model, age, and repair cost. Premium and sports cars cost more to insure.

- Your record — accidents and claims raise the price; a clean history lowers it.

- No-claims history — years without a claim earn a discount (see below).

- Driver age and experience — newer and younger drivers pay more.

- Coverage level and deductible — a higher deductible (the amount you pay per claim) lowers the premium.

- Repair type — "agency repair" (manufacturer workshop) costs more than approved-workshop repair.

How to lower your premium

The cheapest policy is rarely the first one you are shown. A few deliberate choices cut the price without cutting the protection that matters.

- Always compare. Run an aggregator quote at every renewal; the gap between the cheapest and dearest insurer for the same car can be hundreds of riyals.

- Protect your no-claims discount. Pay for small dents yourself rather than reset years of accumulated discount.

- Raise the deductible. Accepting a higher excess per claim lowers the annual premium — sensible if you rarely claim.

- Match repair type to the car. Agency repair is worth it on a new car under warranty; an approved workshop is cheaper on an older one.

- Bundle and pay annually. One yearly payment usually beats monthly instalments, and loyalty or multi-car offers can help.

One realistic example: a driver with three clean years who compares insurers and accepts a moderate deductible can pay markedly less than a neighbour who auto-renews the same car on agency repair with a zero excess. Same vehicle, very different bill.

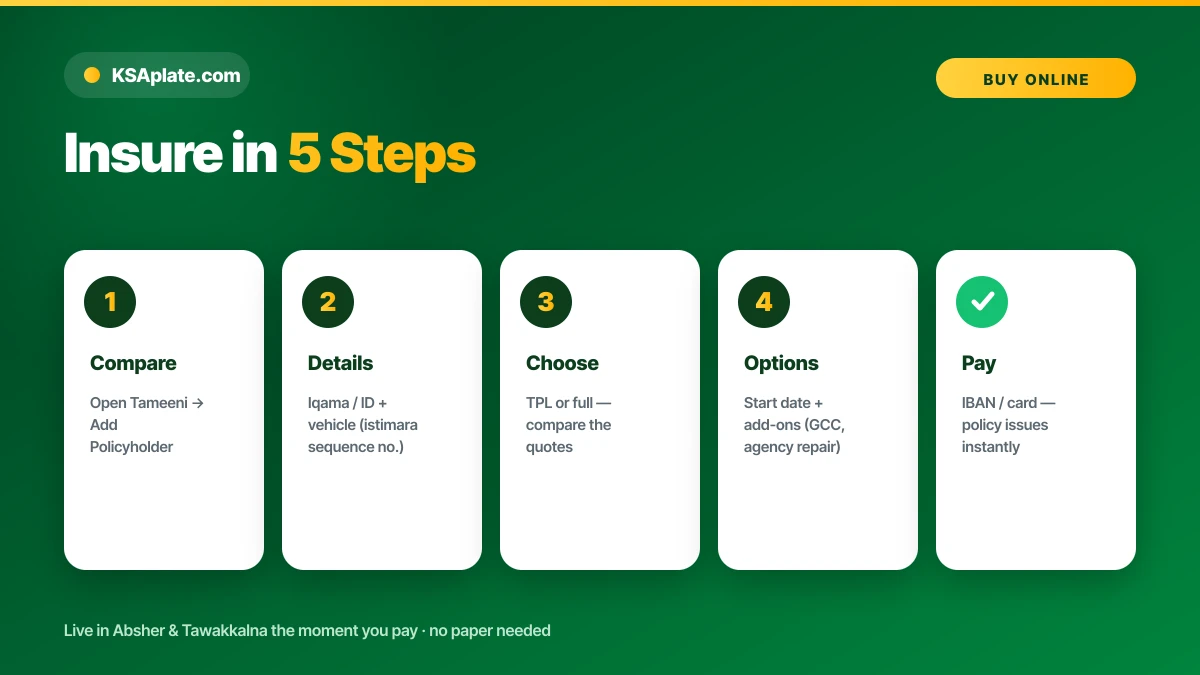

How to buy car insurance online

Buying motor insurance in Saudi Arabia is fully online and takes minutes. The fastest route is a comparison platform that quotes many insurers at once.

- Open an aggregator such as Tameeni (or an insurer's site) and choose Add Policyholder.

- Enter your Iqama or national ID and your vehicle details (the istimara/sequence number).

- Pick the cover type — TPL or comprehensive — and compare the quotes returned.

- Set the policy start date and add any options (GCC cover, agency repair).

- Enter your IBAN, pay, and the policy issues instantly and registers in Absher.

The policy is live the moment you pay. There is no paper to carry — the traffic system reads it directly from the national records.

What you need to buy a policy

The paperwork is light because the insurer pulls most data from your records.

- Your Iqama or national ID number.

- The vehicle registration (istimara) or its sequence number.

- A valid IBAN or card for payment.

- For a transfer, the new owner's details (insurance is in the driver's name).

Insurers and Takaful (Shariah-compliant) cover

Saudi Arabia has a competitive insurance market with many licensed providers, including Tawuniya, Al Rajhi Takaful, Bupa Arabia, MedGulf, Walaa, Gulf Union and Salama. Several operate on a Takaful model — a cooperative, Shariah-compliant structure where members share risk rather than trading it for profit. For buyers who want their cover to align with Islamic finance principles, a Takaful policy delivers the same legal protection through a compliant structure. If that matters to you, our guide to buying a used car pairs naturally with choosing compliant cover at purchase.

No-claims discount (NCD)

A no-claims discount rewards safe driving. For every consecutive year you do not file a claim, insurers lower your renewal premium, often building to a substantial discount after several clean years. The discount is tied to you, not the car, so it follows you when you change vehicles. File a claim and the discount usually resets — which is why drivers often pay small repairs themselves rather than claim and lose years of accumulated NCD.

A no-claims discount can cut a premium sharply. Weigh a small claim against the discount you would lose before you file.

Financed and leased cars

If your car is financed or leased, comprehensive insurance is almost always mandatory. The bank or finance company holds an interest in the vehicle until the loan is settled, so it requires full cover to protect that asset against theft, fire, and accident damage. The policy typically names the financier, and you must keep it active for the life of the loan. Letting it lapse can breach the finance agreement, so align the insurance renewal with the rest of your vehicle paperwork.

Insurance, istimara renewal and Fahes

Insurance is one link in a chain. A valid policy is a prerequisite to renew your istimara and to transfer ownership, and it works alongside the annual Fahes inspection. The clean order for staying road-legal each year is simple: pass Fahes, hold valid insurance, clear any fines, then renew the registration.

Because these steps depend on each other, aligning their dates turns four errands into one. For the next step after insuring, see our guide to renewing the istimara via Absher, and the Fahes periodic inspection guide for the test that precedes it.

Accidents and Najm claims

Najm is the national operator that documents motor accidents and supports insurance claims in Saudi Arabia. After a collision, you report through Najm rather than chasing the other driver's insurer yourself. The basic flow is straightforward.

- Make the scene safe and check for injuries; call emergency services if needed.

- Contact Najm (app or hotline) to log the accident and get a report with fault assigned.

- File the claim with the at-fault driver's insurer, using the Najm report as evidence.

- Follow up until settlement — the regulator targets claim settlement within about 15 working days.

Keep your policy number and the Najm report together; both are needed to move a claim forward quickly.

Driving to the UAE and across the GCC

A standard Saudi policy covers you inside the Kingdom. If you plan to drive to the UAE or elsewhere in the GCC, you need cross-border cover — often arranged as an add-on or a separate "orange card" style extension that extends liability into the neighbouring country. Confirm the exact countries and dates with your insurer before you travel, because driving abroad on a domestic-only policy can leave you uninsured the moment you cross the border. Our car ownership transfer guide covers the related paperwork if you are buying or selling across the region.

Expats and Iqama holders

Expatriates buy car insurance exactly like citizens. You quote and purchase online using your Iqama number, and the policy links to your vehicle the same way. Premiums are based on the car and your driving record, not your nationality. Keep your Iqama valid, because lapsed residency can block the linked services — including the istimara renewal that requires the insurance in the first place.

Buying or selling a vehicle next?

Insurance, inspection and registration all travel with the car. Browse verified listings or value a plate in seconds.

Browse the marketplaceCommon mistakes that cost drivers money

- Buying TPL for an expensive car — one at-fault crash and you fund the repair yourself.

- Auto-renewing without comparing — loyalty rarely beats a fresh aggregator quote.

- Claiming small damage and losing years of no-claims discount.

- Letting cover lapse, which blocks the istimara renewal and risks a fine.

- Driving to the UAE without adding cross-border cover.

- Ignoring the deductible — a low premium with a high excess can cost more after a claim.

Frequently asked questions

Is car insurance mandatory in Saudi Arabia?

How much does car insurance cost in Saudi Arabia in 2026?

What is the difference between TPL and comprehensive?

Does TPL cover damage to my own car?

How do I buy car insurance online?

Do I need comprehensive insurance for a financed car?

How do I claim after an accident?

Can an expat buy car insurance in Saudi Arabia?

Does my Saudi policy cover driving in the UAE?

What is a no-claims discount?

What is Takaful car insurance?

Can I cancel or transfer my car insurance?

Conclusion & next steps

Car insurance in Saudi Arabia comes down to one decision: the legal minimum, or full protection for your own car. Buy TPL to stay road-legal and shield others; choose comprehensive for a newer, financed, or valuable vehicle. Compare insurers on an aggregator, mind the deductible and your no-claims discount, and keep the policy aligned with your Fahes and registration dates. Ready for the next step? Renew your istimara via Absher, or browse the KSAplate marketplace when it is time to buy or sell.