TL;DR:

- Car finance in Saudi Arabia is a Shariah-compliant way to buy a car in monthly installments — the bank profits from a sale or lease, not from interest (riba). The three structures are Murabaha, Ijara and Tawarruq.

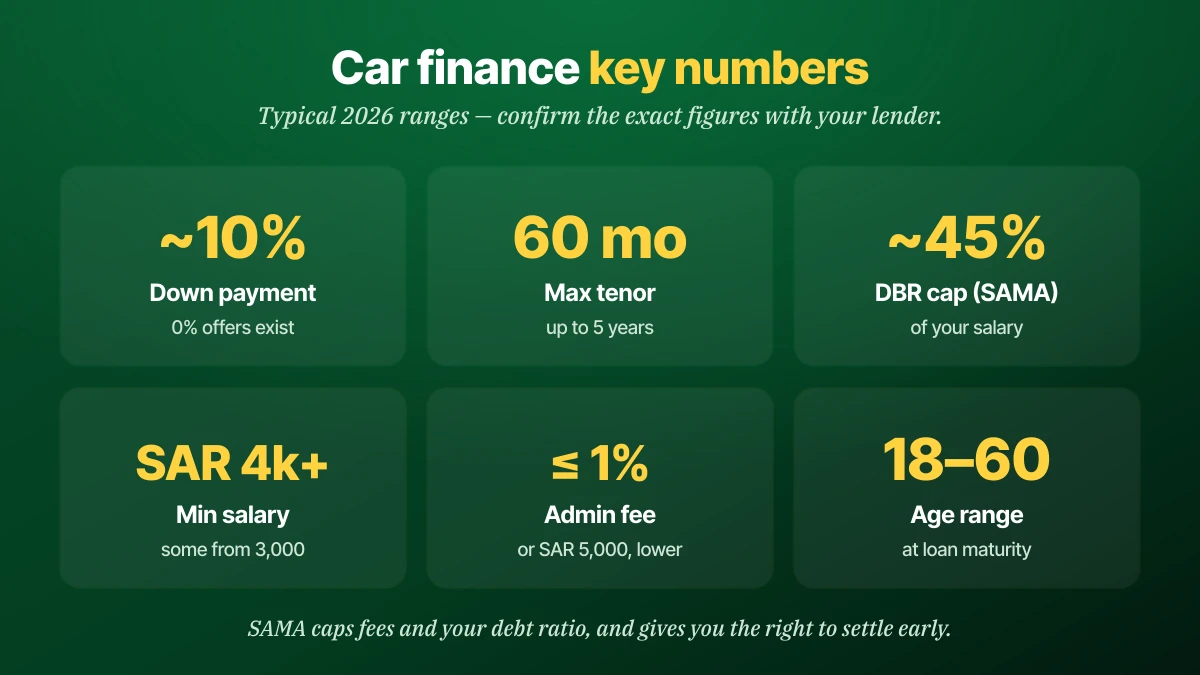

- Typical terms: up to 60 months, a down payment around 10% (some 0% offers), and a final/balloon payment of up to ~25–40% on some plans.

- To qualify you generally need to be 18–60, earn from about SAR 4,000 (some lenders 3,000), pass a SIMAH credit check, and often transfer your salary to the lender.

- SAMA protects you: your total monthly installments are capped (commonly up to ~45% of salary), the admin fee can't exceed 1% or SAR 5,000, and you have the right to settle early.

- Finance the right car, not too much car. Check the vehicle's market value first so your monthly payment fits the budget — then choose the structure with the lowest total cost.

Quick answer: Car finance in Saudi Arabia lets you buy a car in monthly installments through a Shariah-compliant structure — Murabaha, Ijara or Tawarruq — with no interest. Terms run up to 60 months, down payments start around 10%, and you usually need a salary from about SAR 4,000 plus a SIMAH credit check. SAMA caps your debt ratio and fees and lets you settle early.

What car finance is

Car finance in Saudi Arabia is a way to buy a vehicle now and pay for it in fixed monthly installments instead of one cash payment. Because the system is Shariah-compliant, the lender does not charge interest — it earns a profit by selling or leasing the car to you.

That single fact shapes everything. A conventional interest loan does not exist here for retail car buyers; instead a Saudi bank or licensed finance company uses an Islamic contract approved by its Shariah board and regulated by the Saudi Central Bank (SAMA). The cost is real, but it is structured as a markup or rent, not riba.

In plain terms: you agree a total price up front and divide it into months. The art is choosing the structure and term that keep that total — and your monthly payment — as low as possible.

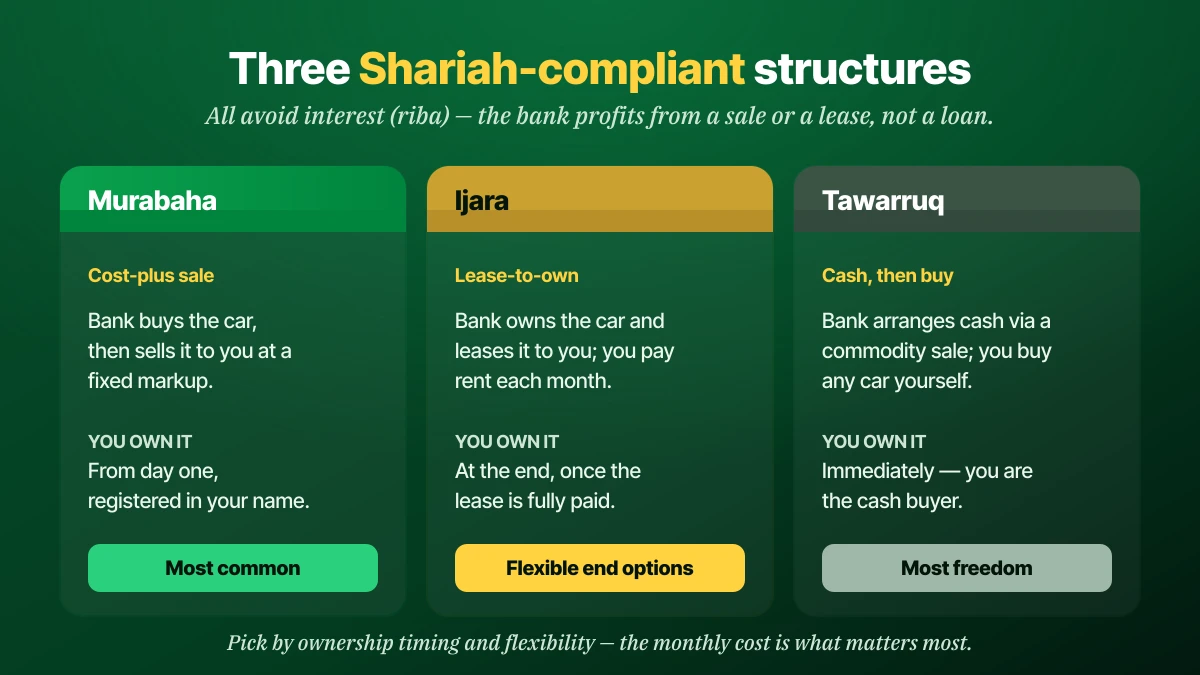

The 3 Islamic structures

Saudi car finance comes in three Shariah-compliant structures, and they differ mainly in who owns the car and when. Understanding them helps you compare offers that look similar on the monthly figure.

| Structure | How it works | You own the car |

|---|---|---|

| Murabaha | Bank buys the car, then sells it to you at cost plus a fixed profit | From day one, in your name |

| Ijara | Bank owns the car and leases it to you; you pay monthly rent | At the end, once fully paid |

| Tawarruq | Bank arranges cash through a commodity sale; you buy any car yourself | Immediately, as a cash buyer |

Murabaha is the most common auto product and registers the car in your name from the start. Ijara (lease-to-own) keeps ownership with the bank until the final payment, which can mean flexible end options. Tawarruq gives you cash to buy any car privately, which suits buying from a private seller. For the plate-buying equivalent of these contracts, see our guide to Saudi licence plate financing.

Who qualifies

Car finance eligibility in Saudi Arabia is a short checklist, and most working residents meet it. Lenders verify each point before approval.

- Age: from 18, and usually no older than 60 when the finance matures.

- Income: a minimum salary commonly between SAR 4,000 and SAR 6,000, though some products start around SAR 3,000.

- Residency: Saudi nationals and expats with a valid Iqama both qualify; expat terms may be tied to Iqama validity.

- Credit record: a SIMAH (Saudi Credit Bureau) check of your existing debts and repayment history.

- Salary transfer: many lenders require your salary to be paid into them; non-transfer options exist at a higher cost.

The deciding factor is rarely your salary alone — it is your debt burden ratio. If existing loans already use most of your allowance, a higher income still won't unlock a bigger car.

What's your car worth?

Get a free instant estimate based on real Saudi market data — then sell it on KSAplate with direct WhatsApp contact.

Value My Car — FreeHow to finance a car in 5 steps

Financing a car follows a standard sequence in Saudi Arabia. Doing the first two steps before you talk to a lender protects you from over-borrowing.

- Know your budget and DBR. Work out the monthly payment you can carry, remembering SAMA caps your total installments at a share of salary.

- Pick the car and check its value. Confirm the market price so you don't finance more than the car is worth — use our guide to how much a used car is worth, and browse cars for sale on KSAplate.

- Compare offers and apply. Look at total cost, not just the monthly figure, across a bank or finance company. A SIMAH credit check runs at this stage.

- Pay the down payment. Often around 10% of the price, though 0%-down offers appear at dealers.

- Sign, insure and register. Comprehensive car insurance is required while financed, and ownership is recorded on Absher. See how ownership transfer works.

If you are buying used, pair this with our used-car buying guide so the car passes inspection before you commit to years of payments.

Down payment, tenor & the balloon payment

Three numbers shape your monthly cost: the down payment, the term (tenor), and any final lump-sum "balloon" payment. Adjusting them trades a lower monthly figure against a higher total.

A down payment of around 10% is common, and a bigger one lowers both your monthly payment and total profit paid. The tenor runs up to 60 months; a longer term cuts the monthly amount but raises the total cost. A balloon (final) payment — allowed up to roughly 25–40% of the price on some plans — keeps monthly payments low, but you must pay or refinance that lump sum at the end. Choose the shortest term and smallest balloon your budget allows to pay the least overall.

What it really costs

The true cost of car finance is the profit plus fees on top of the car price, not the monthly number a salesperson quotes. Always compare the all-in total.

Add three things to the car's price: the finance profit (the markup or rent across the whole term), the administrative fee (capped by SAMA at 1% of the amount or SAR 5,000, whichever is lower), and mandatory comprehensive insurance for the financed period. A car advertised at SAR 80,000 can cost noticeably more once profit, fee and insurance are added over five years.

Put rough numbers on it. Take a car priced at SAR 80,000 with a 10% down payment of SAR 8,000, financing SAR 72,000 over five years. Depending on the profit rate, the total profit might add several thousand riyals, the admin fee up to SAR 720 (1% of the financed amount), and comprehensive insurance a few thousand more across the term. The monthly installment might look comfortable, but the all-in total is what leaves your account — and it can sit thousands above the sticker price.

Two offers with the same monthly payment can have very different totals. Ask for the total amount payable and the total profit in riyals — that single number, not the monthly figure, tells you which finance is cheaper.

New vs used car finance

Both new and used cars can be financed in Saudi Arabia, but used-car finance comes with eligibility limits tied to the vehicle's age and mileage. New-car finance is simpler and usually cheaper.

| Factor | New car | Used car |

|---|---|---|

| Approval | Easier, dealer-supported | Possible, with conditions |

| Profit rate | Often lower / promotional | Usually higher |

| Vehicle limits | None on age | Age (~≤10–12 yrs at maturity) & mileage (~≤80,000 km) caps |

| Down payment | 0%–10% offers | Typically higher |

If you finance a used car, confirm it meets the lender's age and mileage rules before you fall for it, and verify its history first — read our guide on valuing a used car so you don't over-finance a depreciating model.

Salary transfer or not

A salary-transfer requirement means the lender wants your monthly pay deposited with them as a condition of finance. It usually unlocks the best rates, but non-transfer products exist for a higher cost.

Transferring your salary gives the lender security, so it rewards you with a lower profit rate, a smaller down payment, or a longer term. If you cannot or prefer not to move your salary — for example, you bank elsewhere — non-salary-transfer finance is available, but expect a higher rate and stricter terms. Weigh the rate difference against the inconvenience before deciding.

Your rights under SAMA

SAMA, the Saudi Central Bank, regulates all consumer finance and gives borrowers concrete protections. Knowing them stops you overpaying or being trapped.

- Debt burden cap: your total monthly installments cannot exceed a set share of your salary (commonly up to ~45%), preventing over-lending.

- Fee cap: the administrative fee is limited to 1% of the finance amount or SAR 5,000, whichever is lower.

- Early settlement: you have the right to repay early and receive a fair reduction on the remaining profit.

- Transparency: the lender must disclose the total amount payable, the profit, and the annual percentage rate before you sign.

Early settlement is a right, not a favour. If your finances improve, paying the contract off early is the single biggest way to cut the total profit you hand over.

Finance or pay cash?

Financing makes sense when it frees cash you need elsewhere or lets you buy a safer, more reliable car than you could afford outright. Paying cash makes sense when you have the funds and want to avoid all profit and fees.

The honest trade-off is cost versus flexibility. Cash is always cheaper because you pay no profit, admin fee, or mandatory comprehensive insurance markup. Finance spreads the cost and keeps savings intact, but you pay for that convenience. A useful rule: if the finance profit over the term is small relative to what your cash could earn or cover elsewhere, finance; if not, pay cash and avoid the markup entirely. There is also a middle path many Saudi buyers use — a larger down payment with a short term. It keeps most of your savings working, limits the profit you pay, and clears the car quickly, capturing much of the benefit of both options.

Whichever you choose, the decision should follow the car, not the other way round. Pick a reliable model that holds its value, confirm a fair price, and only then decide how to pay for it.

Mistakes that cost you

Most expensive finance mistakes are avoidable and come from focusing on the wrong number. A few habits protect both your budget and your credit record.

- Judging the deal by the monthly payment. A low monthly figure often hides a long term, a big balloon, or a high total. Always ask for the total amount payable.

- Maxing out your debt ratio. Borrowing to the SAMA limit leaves no room for emergencies and can block future finance. Leave a margin.

- Over-financing a fast-depreciating car. If the car loses value faster than you repay, you owe more than it is worth. Value it first.

- Skipping the early-settlement clause. Confirm how early repayment is calculated before signing — it is your biggest lever to cut total cost.

- Ignoring insurance cost. Comprehensive cover is mandatory while financed; factor it into the monthly budget, not as an afterthought.

The cheapest finance is the one you exit early on the right car. Over-borrowing on the wrong car is how a manageable payment becomes a five-year trap.

Frequently asked questions

What is car finance in Saudi Arabia?

Is car finance in Saudi Arabia halal?

What salary do I need to finance a car?

How much down payment do I need?

How long can I finance a car for?

Can expats get car finance in Saudi Arabia?

What is a balloon or final payment?

Can I pay off my car finance early?

Can I finance a used car?

Conclusion & next steps

Car finance in Saudi Arabia is straightforward once you see the shape of it: a Shariah-compliant Murabaha, Ijara or Tawarruq contract that spreads a car's cost over up to five years, with no interest and clear SAMA protections. Decide your budget and debt ratio first, pick the structure with the lowest total cost, and never judge an offer by the monthly figure alone — ask for the total payable. Most of all, finance the right car: check its real value and condition before you commit. Start by finding it — browse verified cars on KSAplate, value it with our used-car value guide, then finance with confidence.