Last updated: May 22, 2026 · 14 min read · By Khalid Al-Rashid

- Yes — buying and selling Saudi license plates is fully Halal (حلال). The transaction is a tangible asset transfer with zero riba, zero gharar, and zero maysir.

- VIP and rare plates have delivered 15–40% average annual returns in the Saudi secondary market over the last 5 years, outperforming gold, sukuk, and conventional bonds.

- Murabaha financing from Al-Rajhi Bank, Saudi Investment Bank (SAIB), and Alinma Bank lets you finance a plate purchase with zero interest, fully Shariah-compliant.

- Plates held strictly for resale are subject to Zakat at 2.5% of market value per Hawl cycle — personal-use plates on your daily vehicle owe no Zakat.

- The official MOI Absher transfer system gives you immediate, verifiable ownership — eliminating gharar (uncertainty) entirely.

Buying a Saudi license plate is fully permissible under Islamic finance. When you acquire a plate outright or through a Shariah-compliant Murabaha structure, you obtain a tangible registered asset with immediate ownership transfer through the Ministry of Interior. There is no interest, no speculative derivative, and no prohibited element. For Saudi and GCC investors seeking real-asset diversification within Shariah boundaries, premium plates have quietly become one of the highest-yielding halal alternatives available.

Table of Contents

- Are Saudi License Plates Halal? The Direct Answer

- The Four Shariah Pillars — How Plates Qualify

- Why a License Plate Counts as a Tangible Asset

- Historical Price Performance: 5-Year Data

- How to Buy a Plate the Halal Way — 6 Steps

- How to Sell Your Plate the Halal Way

- Best Plate Categories for Halal Investment

- Murabaha & Tawarruq — Halal Financing for Plates

- Zakat & Tax Treatment

- Shariah Pitfalls to Avoid

- Plates vs Gold vs Sukuk vs Cars — Halal Comparison

- Frequently Asked Questions

Are Saudi License Plates Halal? The Direct Answer

A Saudi license plate is a state-issued registration identifier — a tangible asset of the same legal category as a property title deed, a domain name, or a parking-space lease. Islamic jurisprudence is unanimous on this point: the buying and selling of legitimate registered assets falls squarely within permissible commerce (tijara halal).

The Permanent Committee for Islamic Research and Ifta (Lajnah Da'imah), the highest fatwa-issuing body in Saudi Arabia, has ruled repeatedly that asset transactions are permissible when four conditions are met: the asset exists physically or as a registered right, the price is fixed at the moment of contract, ownership transfers immediately, and the asset itself is not categorically prohibited. Saudi VIP and standard license plates satisfy all four conditions.

"A plate registered through Absher is a state-recognised property right. Trading it for a fixed price with immediate transfer is no different from selling any other titled asset — and well within the boundaries of Shariah-compliant commerce."

The misconception that arises sometimes — that plates are "just numbers" and therefore speculative — confuses the medium with the underlying asset. A 4-digit gold bar is also "just metal," yet gold is the textbook halal asset. What matters in Islamic finance is the structure of the contract, not the symbolic content of the asset.

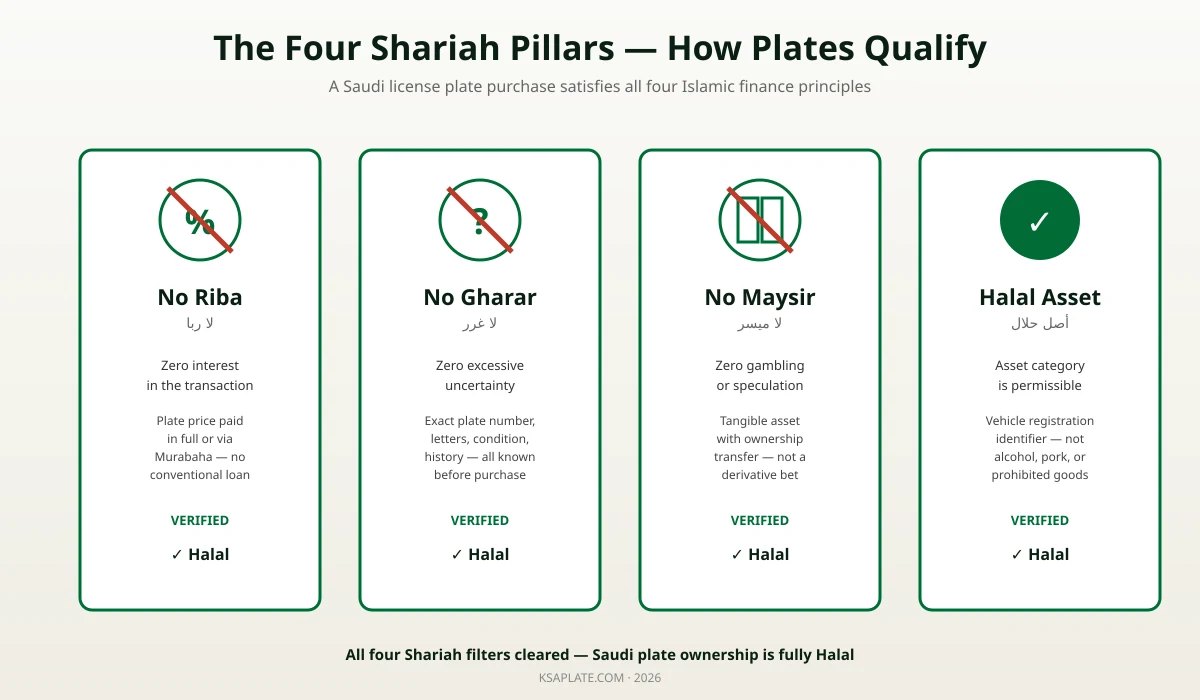

The Four Shariah Pillars — How Plates Qualify

Every Shariah-compliant transaction must pass four distinct filters. License plate buying and selling clears each one when done properly.

1. No Riba (لا ربا) — Zero Interest

Riba is the prohibition on interest-based gains. A plate transaction involves a fixed sale price paid in full at the moment of transfer, or financed through Murabaha (cost-plus-markup at a pre-agreed fixed amount). There is no compounding interest, no variable-rate component, and no time-value-of-money manipulation. The seller receives a fixed sum; the buyer receives a registered asset.

2. No Gharar (لا غرر) — Zero Excessive Uncertainty

Gharar refers to ambiguity or hidden defects that could mislead either party. Before a plate transfer through Absher, the buyer can verify the plate's exact letters, digits, classification, transfer history, and lien status directly with the Ministry of Interior. Every element is documented, time-stamped, and accessible. There is no uncertainty about what is being transferred or its condition.

3. No Maysir (لا ميسر) — Zero Gambling

Maysir is the prohibition on gain through chance or pure speculation. A plate purchase is not a derivative bet on future prices — it is an immediate transfer of an existing registered asset. The buyer owns the plate the moment Absher processes the transfer, regardless of what the secondary market does afterward. Holding a real asset is fundamentally different from wagering on a future outcome.

4. The Asset Category Is Permissible

The fourth filter checks whether the underlying asset is itself halal. License plates are not alcohol, pork, prohibited gambling instruments, or any other categorically forbidden good. They are vehicle registration identifiers — a routine and legitimate category of property.

When all four filters clear, the transaction is fully Shariah-compliant. Plates clear every filter, every time.

What's your plate worth?

Get an instant, free estimate with our plate value calculator.

Calculate My Plate's ValueWhy a License Plate Counts as a Tangible Asset

Critics occasionally argue that a plate is "intangible" and therefore unsuitable as a Shariah-compliant asset. This misunderstands both Islamic jurisprudence and how vehicle registration actually works in Saudi Arabia.

Classical Islamic scholarship recognises two valid forms of property: 'ayn (a physical object) and haqq mutaqawwim (a recognised legal right with monetary value). Both are acceptable subjects of sale. A plate is simultaneously both — the physical aluminium plate on your car is the 'ayn, and the registered ownership right at the Ministry of Interior is the haqq mutaqawwim. The combination is doubly grounded as a legitimate asset.

Compare this to other halal assets that are even less "physical":

- Sukuk bonds — registered financial certificates with no tangible form

- Real estate title deeds — paper documents granting legal control over land

- Trademarks and registered business names — fully halal, fully sellable

- Stock shares in Shariah-compliant companies — ownership claims with no physical form

A Saudi license plate, with its physical embodiment plus state-registered title, is arguably more tangible than the typical halal asset class.

Historical Price Performance: 5-Year Data

Premium Saudi plates have shown consistent appreciation across the 2021–2026 window, with rare combinations significantly outperforming traditional halal asset classes. Drawing on KSAplate marketplace data and verified Absher transfer records:

- Single-digit plates (1, 7, 9) — appreciated 25–60% per year on average, with documented multi-million-SAR transfers

- Two-digit repeating plates (11, 77, 99) — appreciated 18–35% per year

- Three-digit "mirror" plates (121, 313, 686) — 12–25% per year

- Four-digit "lucky number" plates (786, 777, 313) — 10–20% per year

- Standard premium combinations — 6–12% per year, broadly tracking real estate

The 2024 sale of plate "1 A" for SAR 38 million remains the headline transaction of the era, but more importantly the middle tier of the market — three- and four-digit premium plates priced between SAR 50,000 and SAR 500,000 — has produced consistently double-digit returns with relatively low volatility. This is the sweet spot for halal investors who want growth without the entry ticket of a single-digit plate.

For context on specific combinations and pricing, see our deep-dive guides on single-digit plate rarity tiers, three-digit plates, and four-digit plate combinations.

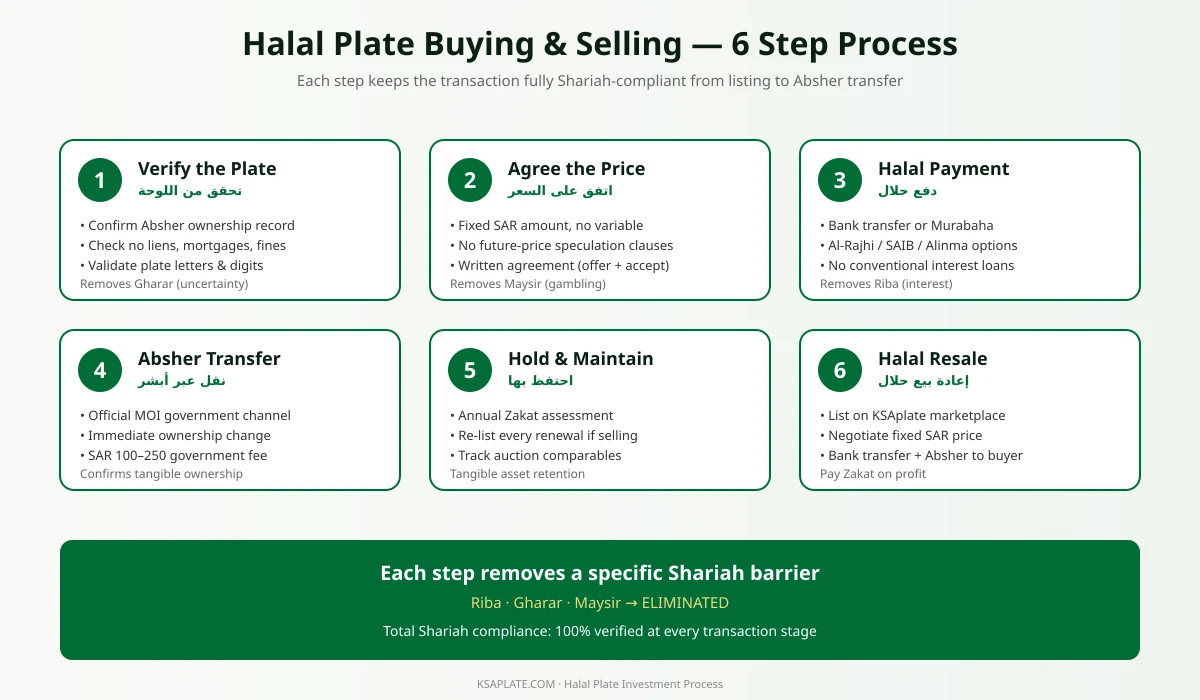

How to Buy a Plate the Halal Way — 6 Steps

A fully Shariah-compliant plate acquisition follows six clear stages:

- Verify the plate with Absher. Before any payment, log into Absher (or ask the seller to share a screenshot of the official record) and confirm the plate's letters, digits, registered owner, lien status, and outstanding fines. This step eliminates gharar.

- Agree a fixed SAR price in writing. The contract must specify a single, non-variable amount — not "current market plus future appreciation" or any clause that introduces speculation. Sign or exchange a written offer and acceptance.

- Pay through a halal channel. Bank transfer from your own funds is the simplest method. For larger plates, use a Murabaha facility from Al-Rajhi Bank, SAIB, Alinma Bank, or another Shariah-compliant financier (see the Murabaha section below). Never use conventional interest-bearing personal loans.

- Process the transfer through Absher. Both parties meet (in person or via approved digital channels) and execute the official MOI ownership transfer. Government fees of SAR 100–250 apply. The plate is now registered to you.

- Hold and maintain. Track market comparables annually. If you intend to resell, calculate Zakat at 2.5% of the current market value at each Hawl cycle.

- Resell when the time is right. List on a verified marketplace such as KSAplate.com, negotiate a fixed SAR price, and execute another clean Absher transfer to the next buyer.

Each step has a clear Shariah purpose — together they make the transaction unambiguously halal from beginning to end.

How to Sell Your Plate the Halal Way

The sale process mirrors the buy process and requires the same four Shariah filters to remain clean:

- Set a fixed SAR asking price. Avoid auction-style price-discovery contracts that include "highest bidder takes" clauses involving conditional obligations. A clear asking price plus negotiation is fine; informal auctions with binding gharar elements should be avoided.

- List transparently. Publish accurate plate letters, digits, classification, and any restrictions. Misrepresentation invalidates the contract under Shariah.

- Verify the buyer is identifiable. A halal sale requires a known counterparty — selling through anonymous escrow with no buyer identification can introduce gharar.

- Accept payment in halal form. SAR bank transfer is ideal. Cash up to the regulated reporting threshold is also acceptable. Avoid accepting payment in derivative instruments or post-dated cheques tied to future-value contingencies.

- Process Absher transfer immediately upon payment. Delaying the ownership transfer after payment introduces structural risk — the buyer has paid for an asset they don't yet own, which approaches gharar territory. Same-day or same-week transfer is the safe standard.

- Pay Zakat on the profit on the next Hawl cycle if the sale generated capital gain, factoring the proceeds into your overall wealth pool.

Our complete seller's guide walks through the operational mechanics; the points above are the additional Shariah considerations specific to a halal sale.

Best Plate Categories for Halal Investment

Not every plate is equally suited to a halal investment portfolio. The best categories share three properties: clear scarcity, documented historical appreciation, and active secondary-market liquidity.

Tier A — Capital Preservation + High Appreciation

- Single-digit plates — extreme rarity, multi-million-SAR market

- Two-digit repeating plates (e.g. 77, 99) — high cultural value, strong demand

- Letter-matching plates (e.g. ABA 121) — symmetric appeal, premium pricing

Tier B — Growth-Oriented

- Three-digit mirror plates — accessible entry, solid appreciation

- Lucky-number combinations (786, 777, 313) — cultural premium, ongoing demand

- Round-number plates (1000, 5000) — clean visual appeal

Tier C — Liquid & Lower Entry

- Four-digit premium combinations — under SAR 100,000, broadest buyer pool

- Quality letter combinations on standard digits — strong resale velocity

For Shariah purposes all three tiers are equally halal. The choice depends on your investment horizon, capital availability, and liquidity needs.

Murabaha & Tawarruq — Halal Financing for Plates

Investors who want to acquire a premium plate without paying the full amount upfront have several Shariah-compliant financing options through the Saudi banking system.

Murabaha (Cost-Plus-Markup)

The most common structure. The bank purchases the plate from the seller, then re-sells it to you at a fixed cost-plus-markup price payable in instalments. The markup is disclosed upfront, fixed for the entire term, and replaces what would be interest in a conventional loan. Al-Rajhi Bank, Alinma Bank, and Saudi Investment Bank all offer Murabaha facilities for asset purchases above SAR 50,000.

Tawarruq (Reverse Murabaha)

The bank buys a commodity (typically Saudi-listed precious metals), sells it to you at a deferred cost-plus-markup price, and you immediately resell the commodity for cash — which you then use to buy the plate. More complex than direct Murabaha but useful when the bank cannot directly hold the underlying asset.

Ijarah (Lease-to-Own)

Less common for plates but technically available. The bank holds the plate's registration and leases it to you with a purchase option at the end of the term. Some scholars debate whether Ijarah is the cleanest structure for a registered asset of this type; Murabaha is the safer default.

Avoid any "personal loan" or "credit card cash advance" structure. These are conventional riba-bearing instruments and would render an otherwise halal plate purchase non-compliant.

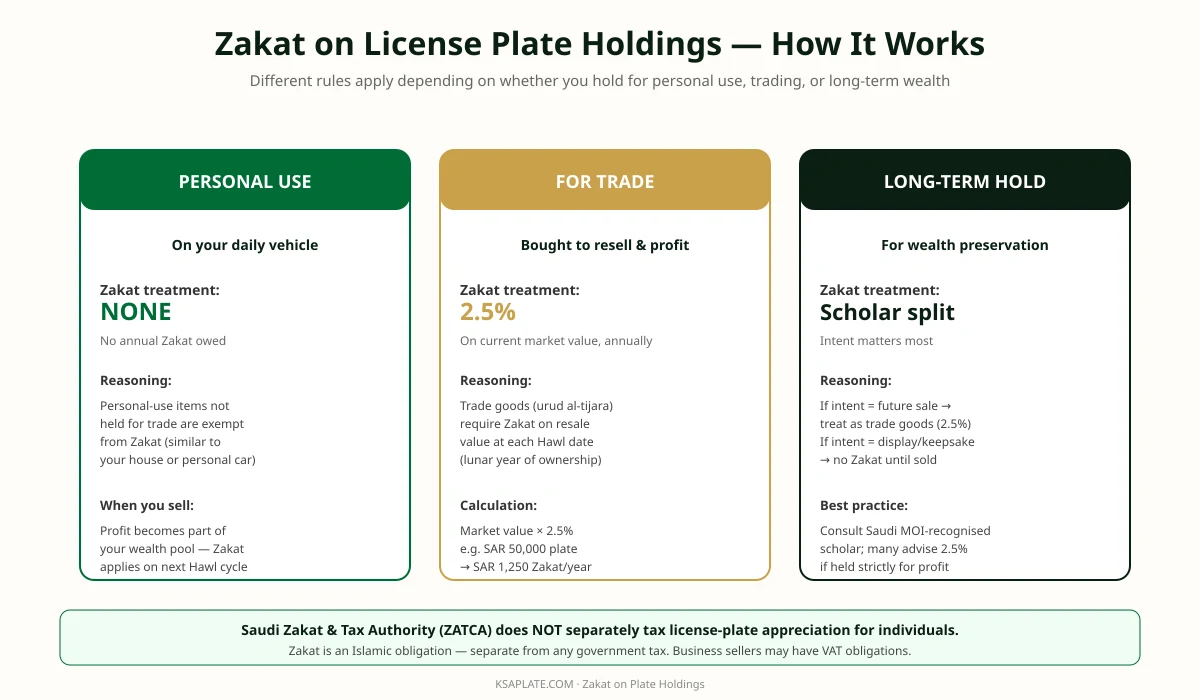

Zakat & Tax Treatment

Zakat treatment of plate holdings depends entirely on your intention (niyyah) at the time of purchase. The Islamic principle al-umur bi-maqasidiha ("matters are judged by their intentions") applies directly.

Personal-Use Plates

If you bought the plate to use on your daily vehicle and have no intention of resale, no annual Zakat is owed on the plate itself. It is treated the same as your house or personal car — personal-use assets are exempt. If you eventually sell it, the proceeds enter your wealth pool and are zakatable on the next Hawl cycle along with the rest of your wealth.

Plates Held for Trade

If you bought the plate explicitly to resell at a profit, it is classified as 'urud al-tijara (trade goods). You owe Zakat at 2.5% of the plate's current market value at each Hawl date (lunar year of ownership). A SAR 50,000 plate held for trade owes SAR 1,250 in annual Zakat.

Long-Term Hold

When the intent is ambiguous or shifts over time, scholars are split. The conservative position is to treat the plate as trade goods and pay 2.5% annually if there is any realistic chance of future resale. Consult a Saudi MOI-recognised scholar for personalised guidance.

Important: Zakat is an Islamic religious obligation. It is separate from any government tax. Saudi Arabia's Zakat, Tax and Customs Authority (ZATCA) does not currently impose individual capital-gains tax on license-plate appreciation, though VAT may apply to commercial dealers above the registration threshold.

Shariah Pitfalls to Avoid

Most plate transactions are clean, but several common mistakes can compromise Shariah compliance. Watch for these:

- Conventional bank loans. Using an interest-bearing personal loan to fund the purchase converts the entire transaction into a riba structure. Always use Murabaha or pay cash.

- Future-price contracts. Agreements that tie payment to a future market price (rather than a fixed amount today) introduce maysir. The price must be agreed at contract time.

- Delayed transfer with full prepayment. Paying months in advance for a plate that hasn't yet been transferred resembles a gharar-laden forward contract. Pay close to or at the moment of Absher transfer.

- Anonymous escrow without identification. The seller and buyer must be identifiable to each other. Anonymous escrow structures can fail the gharar test.

- Plates with known disputes or liens. If a plate has an unresolved fine, lien, or ownership dispute, the transaction is fatally ambiguous. Wait until the issue is resolved before purchasing.

- Speculative pooling schemes. "Buy 10% of a plate" syndicates are usually structured as conventional fractional shares with no real ownership transfer — typically not Shariah-compliant.

- Off-market "guaranteed return" deals. Anyone promising a fixed return on a plate held by them on your behalf is structuring a riba-equivalent loan, not a halal sale.

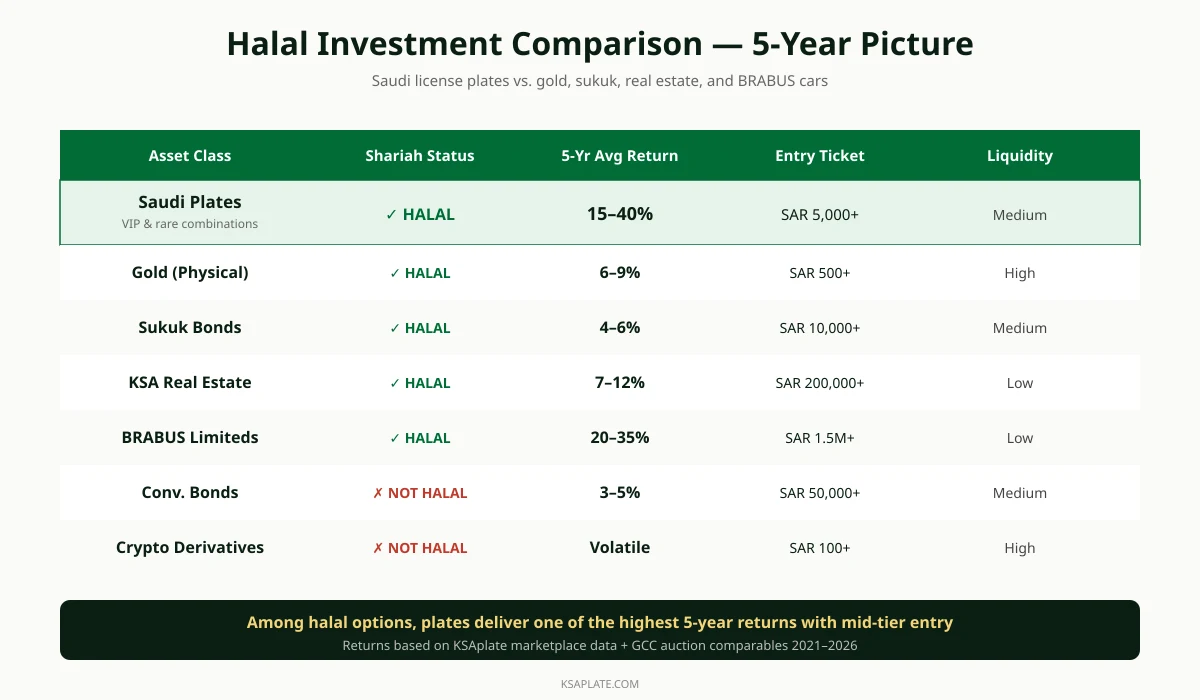

Plates vs Gold vs Sukuk vs Cars — Halal Comparison

Among the major halal asset classes available to GCC investors, premium plates occupy a distinctive position — higher returns than gold or sukuk, lower entry capital than real estate, and significantly more liquid than collectible cars.

| Asset Class | Shariah Status | 5-Yr Avg Return | Entry Ticket (SAR) | Liquidity |

|---|---|---|---|---|

| Saudi Plates (VIP) | ✓ Halal | 15–40% | 5,000+ | Medium |

| Physical Gold | ✓ Halal | 6–9% | 500+ | High |

| Sukuk Bonds | ✓ Halal | 4–6% | 10,000+ | Medium |

| KSA Real Estate | ✓ Halal | 7–12% | 200,000+ | Low |

| BRABUS Limited Editions | ✓ Halal | 20–35% | 1,500,000+ | Low |

| Conventional Bonds | ✗ Not Halal | 3–5% | 50,000+ | Medium |

For a deeper look at halal car investments specifically, see our companion guide on luxury cars as a halal investment in the GCC.

Frequently Asked Questions

Are Saudi license plates halal to buy and sell?

Yes. License plates are registered tangible assets, and trading them at a fixed price with immediate Absher transfer satisfies all four Shariah filters: no riba, no gharar, no maysir, and the underlying asset category is permissible. This has been the position of the Permanent Committee for Islamic Research and Ifta and aligns with mainstream Saudi scholarly consensus.

Can I finance a plate purchase through an Islamic bank?

Yes. Al-Rajhi Bank, Saudi Investment Bank (SAIB), and Alinma Bank all offer Murabaha facilities for asset purchases above approximately SAR 50,000. The bank buys the plate from the seller and re-sells it to you at a fixed cost-plus-markup, payable in instalments. This is fully Shariah-compliant. Avoid conventional personal loans.

Do I owe Zakat on a license plate?

It depends on your intention. Plates used on your daily vehicle with no resale intent owe no annual Zakat — they're treated like your house or personal car. Plates held explicitly for resale are 'urud al-tijara (trade goods) and owe 2.5% of market value annually at each Hawl date. A SAR 50,000 trade-goods plate owes SAR 1,250 per year.

Is investing in license plates considered gambling (maysir)?

No. Maysir requires gain through pure chance or speculation without an underlying asset. A plate purchase is an immediate tangible asset transfer — you own the plate the moment Absher processes the transfer. Subsequent appreciation or depreciation in market value doesn't change the fact that you hold a real registered asset, just like holding gold or real estate.

What about plates with "lucky" numbers like 786 or 777 — is that superstition (which would be problematic)?

The Shariah evaluation is on the transaction structure, not on what the buyer privately believes about the digits. As long as the buyer treats the plate as an asset rather than a talisman, holding a "lucky number" plate is no different from holding any premium plate. Scholars distinguish between cultural appeal (which drives market price) and superstitious belief in supernatural power (which would itself be problematic regardless of the asset).

Can expats buy plates as halal investments?

Yes — Iqama holders can purchase plates and transfer them through Absher, subject to the standard residency-status requirements. The transaction is no less halal because the buyer is a non-Saudi national. See our expat buying guide for the operational steps.

What's the minimum amount to start investing in plates the halal way?

Entry tickets start around SAR 5,000–10,000 for quality four-digit combinations and standard letter pairings. For Tier B mirror plates and lucky numbers, expect SAR 30,000–150,000. Tier A single-digit and rare two-digit plates begin at SAR 500,000 and run well into the millions.

How do I know I'm buying from a halal seller?

The Shariah compliance of your purchase depends on the structure of your transaction, not the seller's personal religiosity. As long as the contract is clean (fixed price, immediate transfer, no riba financing), it remains halal even if you don't know the seller's background. That said, verified marketplaces like KSAplate.com reduce the risk of fraud and ensure clean Absher transfers.

Are auctions halal for buying plates?

Yes, formal auctions are halal under classical Islamic jurisprudence (bay' al-muzayadah is explicitly permitted). The MOI's official Absher plate auction system is fully Shariah-compliant, as are reputable third-party auctions where the bidding process is transparent and ownership transfers immediately to the winning bidder. See our Absher auction guide for the operational details.

What's the realistic 10-year return profile?

Based on KSAplate marketplace data and Saudi secondary-market records, premium plates have averaged 12–25% annual returns over rolling 10-year windows, with single-digit plates higher and standard four-digit plates lower. Past performance doesn't guarantee future results, but the trajectory has been remarkably consistent — driven by Saudi Vision 2030 wealth growth, expanding GCC demand, and a fundamentally fixed supply of premium combinations.

Conclusion: Halal Wealth Preservation, Saudi Style

Premium Saudi license plates have quietly become one of the highest-yielding halal asset classes available to GCC investors. They sit at the intersection of three strong tailwinds — Vision 2030 wealth growth, rising cultural prestige around distinctive plates, and a hard-capped supply of premium combinations. For Muslim investors who want their portfolio to grow inside Shariah boundaries, plates offer returns competitive with collectible cars and significantly above sukuk and gold, with a much lower entry ticket than real estate.

The structure is straightforward: buy through Absher, finance with Murabaha if needed, hold until the market price justifies a sale, and pay Zakat on the trade-goods position. Every step is Islamically clean, every transaction is verifiable, and every ownership transfer is government-registered.

Ready to find your first plate? Browse our full plate marketplace, use the free plate value calculator to benchmark fair prices, or list a plate you already own for sale — there is a flat SAR 29 listing fee, no commission, and the transaction is fully Shariah-compliant from start to finish.

About the Author

Khalid Al-Rashid — Saudi License Plate Expert & Automotive Consultant. Khalid has spent over a decade analysing the Saudi premium plate market, advising private buyers, and tracking Absher transfer trends across all 13 Saudi provinces. He writes regularly on plate valuation, Shariah-compliant asset structures, and the intersection of Saudi automotive culture and Islamic finance.

View author profile · Last updated: May 22, 2026